Why Choosing the Right Mortgage Matters When Buying a Home in Saskatoon

Buying a home is one of the biggest financial decisions most Canadians will ever make, and choosing the right mortgage plays a major role in long-term affordability. Understanding the basics—like interest rates, payment structure, and loan terms—can help you make a confident and informed decision from the start.

Interest Rates and Amortization

One of the first things to consider is the type of interest rate. Fixed-rate mortgages offer stability with consistent payments over time, while variable-rate mortgages can fluctuate with market conditions, potentially saving money—or costing more—depending on rate changes. It’s important to weigh your risk tolerance and financial flexibility when deciding between the two.

Another key factor is the amortization period, which is the total length of time it will take to pay off your mortgage. A longer amortization means lower monthly payments but more interest paid over time, while a shorter period increases monthly costs but reduces the total interest expense. Finding the right balance is crucial based on your budget and long-term goals.

Payments and Terms & Conditions

Payment frequency is often overlooked, but it can have a meaningful impact. Options like accelerated bi-weekly payments can help you pay down your mortgage faster and save on interest compared to standard monthly payments.

Finally, it’s important to understand the terms and conditions of your mortgage, including penalties for breaking the contract, prepayment options, and flexibility if your financial situation changes. Not all mortgages are created equal, and the fine print can make a significant difference.

Taking the time to understand these components can help you avoid costly mistakes and potentially save thousands of dollars over the life of your mortgage.

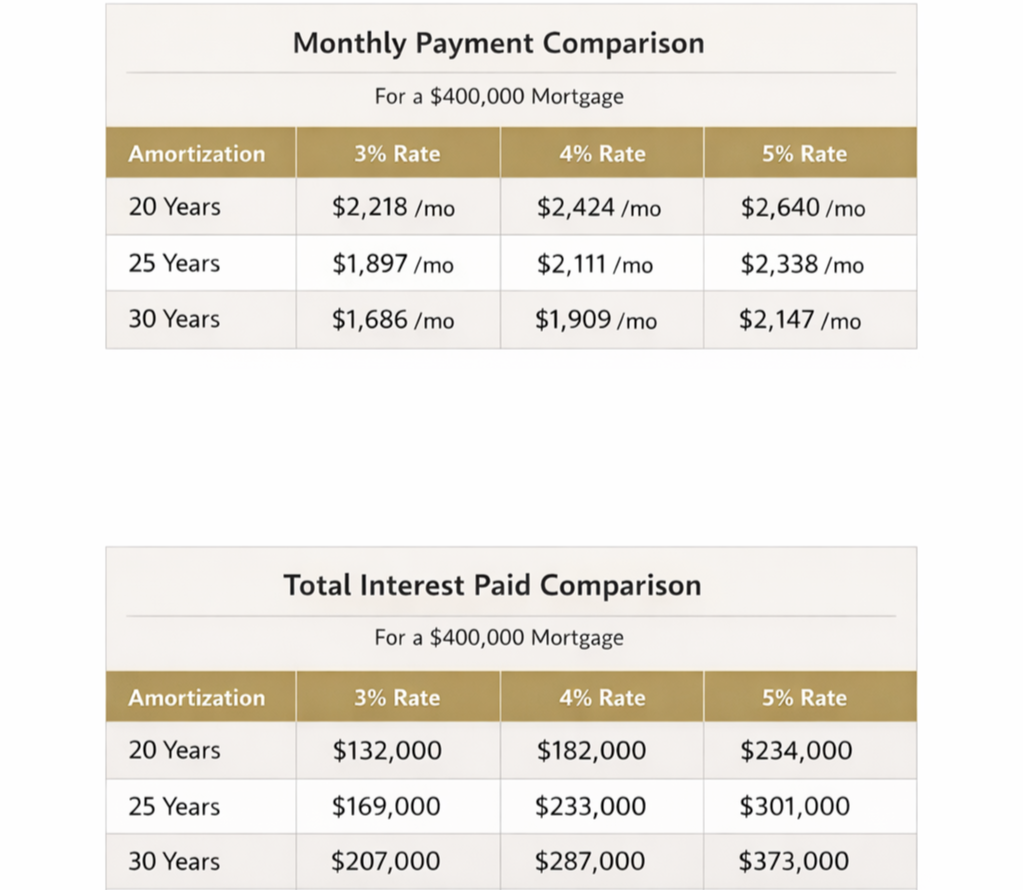

Here’s a simple way to understand how mortgage choices impact your finances using a $400,000 home purchase.

Let’s assume a full mortgage amount of $400,000 (for simplicity) and compare amortization periods of 20, 25, and 30 years at interest rates of 3%, 4%, and 5%.

2 tables showing the difference in payments and interest paid depending on amortization period and interest rate.

What This Means

A lower interest rate makes a major difference. For example, on a 25-year mortgage, going from 3% to 5% increases your monthly payment by about $440—and costs you over $130,000 more in interest over time.

Amortization also plays a big role. Moving from a 30-year to a 20-year mortgage at 4% increases your monthly payment by about $500, but saves you roughly $100,000+ in interest.

Key Takeaway

Your mortgage isn’t just about what you can afford monthly—it’s about the total cost over time. Even small changes in interest rates or amortization can mean tens (or hundreds) of thousands of dollars in difference, which is why understanding your options upfront is so important.

306.370.8474 | hello@morrison87.com | @morrisonrealty87